Running a medical practice means walking a tightrope every single day. On one side, you have the non-negotiable duty of providing compassionate, patient-first care. On the other, you have the equally critical need to maintain a healthy cash flow to keep the lights on. The friction between these two priorities often surfaces in one of the most challenging areas: patient collections.

A patient financial policy is a formal document that clearly outlines a medical practice’s procedures for collecting payments, including co-pays, deductibles, and outstanding balances. It defines patient responsibilities, insurance billing processes, and options for delinquent accounts to ensure financial transparency and consistent cash flow. But what most people don’t realize is that the document itself is only half the battle.

Your team spends countless hours chasing unpaid balances, leading to staff burnout and awkward interactions that can erode patient relationships. Every delayed payment strains your practice’s finances, while inconsistent collection efforts create confusion and leave money on the table. This isn’t just a financial leak; it’s an operational bottleneck and a direct threat to patient retention.

A clear, consistent, and empathetically enforced Patient Financial Policy is the bedrock of a healthy revenue cycle. This guide, based on current 2026 healthcare regulations like the No Surprises Act and updated FCRA rules, will not only give you a compliant template but also show you how to solve the enforcement problem for good.

Why a Weak Financial Policy Is Costing Your Practice More Than Just Money?

The red ink on your aging A/R report is often the most visible symptom, but the damage from an inconsistent or poorly enforced financial policy runs much deeper. It quietly drains your practice’s most valuable resources: time, morale, and patient trust.

A vague policy leads to unpredictable cash flow, making it impossible to budget for growth, new equipment, or even payroll with confidence. This financial instability is directly tied to an immense operational drag. Your front-desk staff, who should be focused on creating a welcoming patient experience, are forced to become part-time bill collectors, spending hours on the phone that could be dedicated to care coordination. This constant pressure contributes to burnout and high turnover.

Ultimately, this inefficiency damages the patient experience. When rules are applied inconsistently—some patients are asked for co-pays while others aren’t, or follow-up on outstanding balances is sporadic—it creates frustration and confusion. Patients lose trust, and the therapeutic relationship can be strained by what feels like an arbitrary and stressful financial process. This is the hidden cost that impacts your practice’s long-term health and reputation.

The 7 Core Components of a Compliant & Effective Financial Policy

At first glance, this might seem like just more paperwork. But in reality, a well-structured policy is a tool for creating clarity and fairness for everyone involved. It’s not about being rigid; it’s about being transparent. Here are the seven essential clauses every policy must include.

1. Clear Patient Responsibility Clause

This is the foundational statement. It must explicitly state that the patient (or their guarantor) is ultimately responsible for all charges for services rendered, regardless of their insurance coverage. It sets the stage for all other terms and prevents future disputes about who owes what.

2. Point-of-Service (POS) Collection Mandate

To dramatically improve cash flow and reduce A/R days, your policy must require payment of co-payments, deductibles, and any known outstanding balances at the time of service. This simple, non-negotiable step is one of the most effective levers in a healthy revenue cycle management (RCM) strategy.

3. Insurance & Verification Protocol

This section outlines the patient’s duty to provide current, accurate insurance information before each visit. It should also clarify that while you will bill their insurance as a courtesy, the patient is responsible for understanding their own benefits, including limitations and non-covered services.

4. Policy on Non-Covered Services

Clearly state that services deemed not medically necessary or not covered by a patient’s plan are their full financial responsibility. This is crucial for managing expectations around elective procedures, cosmetic treatments, or services that require prior authorization.

5. Terms for Self-Pay & Uninsured Patients (Good Faith Estimate)

Your policy must detail the process for uninsured and self-pay patients, including any prompt-pay discounts offered. Critically, it must also mention their right to a Good Faith Estimate under the No Surprises Act, ensuring you remain compliant.

6. Delinquent Account Escalation Process

Transparency is key to maintaining patient trust, even with delinquent accounts. Define the exact timeline for an overdue balance—for example, what happens after 30, 60, and 90 days. This clause should state the point at which an account may be turned over to a third-party collection agency, after multiple good-faith contact attempts have failed.

7. Financial Hardship & Payment Plan Options

Compassion is not at odds with good financial practice. Offering clear options for patients facing genuine financial hardship, such as structured payment plans, shows goodwill and makes it more likely you’ll recover the balance over time without alienating the patient.

The Real Challenge: A Great Policy is Useless Without Empathetic Enforcement

Here’s the thing most consultants and DIY templates won’t tell you: writing the policy is the easy part. The real reason collections fail and A/R days balloon is a breakdown in day-to-day execution.

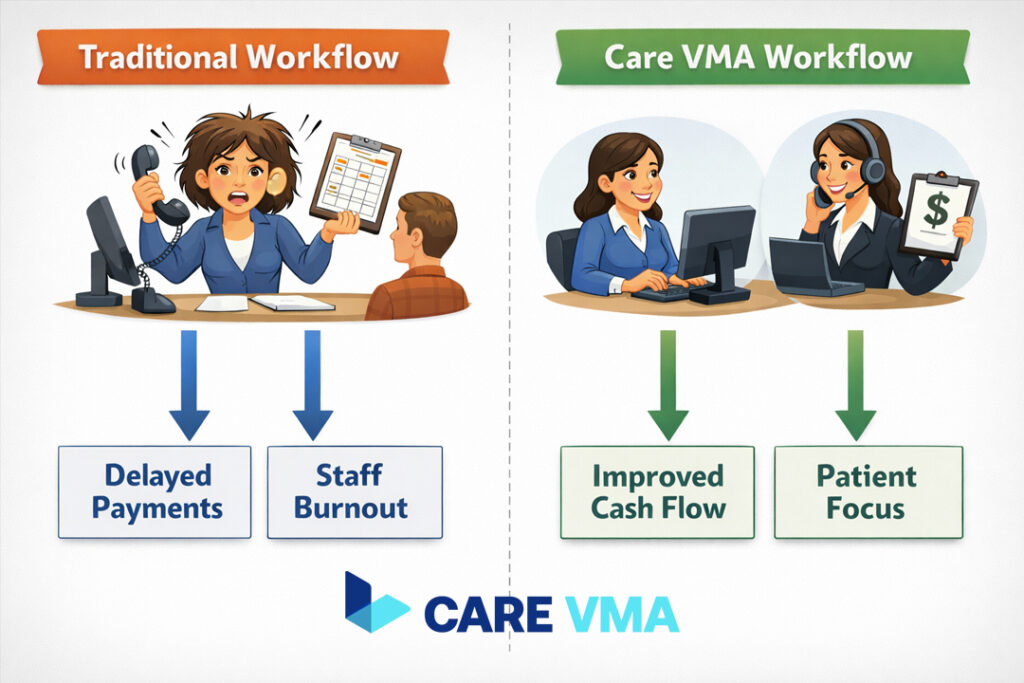

Your front-desk staff are the face of your practice. They are hired for their empathy, scheduling prowess, and ability to manage a busy waiting room—not for their skills in debt collection. Asking them to pivot from a warm welcome to a firm financial conversation is a recipe for inconsistency and stress. They often lack the training in using empathetic scripts, feel uncomfortable having difficult conversations, and are rightly afraid of damaging the patient relationship they just helped build.

This creates a cycle of avoidance. The co-pay isn’t collected, the follow-up call is postponed, and the outstanding balance gets older. The policy sitting in a binder becomes meaningless because the human element—the consistent, professional, and empathetic enforcement—is missing.

The Solution: How Trained VMAs Execute Your Financial Policy Flawlessly

What if the person responsible for upholding your financial policy was a dedicated professional operating outside the emotional dynamics of the clinic? This is where a trained Virtual Medical Assistant (VMA) transforms your revenue cycle from a point of stress into a streamlined, professional system.

A great policy needs a great system to run it. Care VMA provides that system.

- Saves Time: A VMA takes over the incredibly time-consuming tasks that bog down your front office. This includes pre-visit insurance verification, sending payment reminders, making follow-up calls on outstanding balances, and setting up payment plans. This frees your in-house team to focus entirely on the patients in front of them.

- Reduces Burden: Our VMAs are trained specifically in healthcare finance communication. They use proven, empathetic scripts to handle difficult conversations with professionalism and compassion, removing the emotional and mental burden from your clinical staff. They become the consistent, reliable point of contact for all billing inquiries.

- Increases Efficiency: A dedicated VMA ensures your financial policy is applied consistently and fairly to every single patient, every single time. There are no exceptions or forgotten follow-ups. This consistency drastically reduces A/R days, boosts Point-of-Service collections, and stabilizes your practice’s cash flow.

A busy pediatric practice, for example, tasked a Care VMA with handling all pre-visit balance checks and managing incoming calls about payment plans. Within 90 days, their POS collections increased by 40% and overdue balances decreased by 60%—all while their front-desk team reported significantly lower stress levels.

Your Customizable Patient Financial Policy Template

A policy is your starting point. The template below includes all the critical components discussed. Think of it as the “what.” A dedicated VMA from Care VMA is the “how”—the expert resource that brings this document to life and ensures it works for you day in and day out.

Copy and adapt this text for your practice. Information in [brackets] should be customized.

[Practice Name] Financial Policy

Thank you for choosing [Practice Name]. We are committed to providing you with the best possible care. To maintain this standard, we require a clear understanding of our financial relationship. Please read and sign this policy prior to your treatment.

1. Insurance Responsibility Your insurance plan is a contract between you and your insurer. As a courtesy, we will bill your insurance carrier for you. However, you are responsible for any portion of the bill not covered by insurance. If your insurance company does not remit payment within [45] days, the full balance will become your direct responsibility.

2. Proof of Insurance All patients must provide a current, valid insurance card at every visit. If we cannot verify your coverage, you will be treated as a “Self-Pay” patient and will be expected to pay for the visit in full at the time of service.

3. Co-payments, Deductibles, and Balances All co-payments, deductibles, and past-due balances are due in full at the time of service. We accept cash, check, and all major credit cards.

4. Non-Covered Services You are responsible for the full payment of any services deemed “non-covered” or “not medically necessary” by your insurance provider. We encourage you to be familiar with your plan’s benefits and exclusions.

5. Claims for Uninsured (Self-Pay) Patients In accordance with the No Surprises Act, uninsured patients are entitled to a Good Faith Estimate of expected charges. We offer a [e.g., 20%] prompt-pay discount for self-pay accounts paid in full at the time of service.

6. Missed Appointments / Late Cancellations We require at least [24] hours’ notice for all appointment cancellations. Failure to provide adequate notice will result in a fee of $[Amount]. This fee is not billable to insurance.

7. Delinquent Accounts An account is considered past due after [30] days. If an account remains unpaid after [90] days and no payment arrangements have been made, it may be referred to an external collection agency. You will be responsible for any additional collection or legal fees.

8. Financial Hardship If you are experiencing financial difficulties, please speak with our billing specialist. We offer structured payment plans for those who qualify.

I have read, understand, and agree to the terms of this Financial Policy.

Patient/Guarantor Signature Date

Staying Compliant: Key Regulations to Know for 2026

A strong policy protects your cash flow. A compliant one protects your entire practice from legal and financial risk. Here are the key regulations governing patient collections.

The No Surprises Act & Good Faith Estimates

As established by the Department of Health and Human Services, this federal law protects patients from surprise medical bills for out-of-network emergency care. Critically for day-to-day operations, it also mandates that you provide a “Good Faith Estimate” of costs to any uninsured or self-pay patient before their scheduled service.

Fair Debt Collection Practices Act (FDCPA)

While the FDCPA primarily governs third-party collection agencies, its principles are best practice for any practice. It prohibits harassment and false statements when attempting to collect a debt. Adhering to these standards protects your reputation and prevents patient complaints.

Fair Credit Reporting Act (FCRA) Medical Debt Rules

Recent changes to the FCRA significantly impact medical debt reporting. According to the Consumer Financial Protection Bureau, as of 2023, paid medical collection debt can no longer appear on credit reports. Furthermore, medical debts under $500 cannot be reported, and any new medical debt can only be reported after it is at least one year delinquent. Your policy’s escalation timeline must reflect these rules.

Explore Further: Optimizing Your Revenue Cycle

A solid financial policy is just one part of a well-run practice. To see how a remote professional can streamline other administrative functions, explore our guide on what a virtual medical assistant is and what they can do for your practice.

For a deeper look into how our trained specialists can specifically manage your billing and collections process from end to end, visit our Medical Billing Virtual Assistant service page.

FAQ

How do you introduce a new financial policy to existing patients?

The best practice is to announce the policy 30-60 days in advance via email, your website, and in-office signage. Frame it as an effort to improve transparency and create a smoother financial experience. Have all patients review and sign the new policy at their next scheduled visit.

What is the best way to collect past-due balances from patients?

A proactive, multi-channel, and empathetic approach works best. This involves a sequence of automated text/email reminders followed by a personal phone call from a trained professional. The goal is to offer solutions like a payment plan before the account becomes seriously delinquent, preserving the patient relationship.

Can a medical practice send a patient to collections?

Yes, but this should be the final step after multiple, well-documented attempts to collect the debt have been made. Your financial policy must clearly state the timeline (e.g., after 90 or 120 days of non-payment) and the conditions under which an account will be transferred to a third-party agency.

Conclusion

A strong financial policy is much more than a document—it’s an essential system for ensuring the financial health of your practice and maintaining patient trust. But a system is only as good as the people who run it.

It’s time to stop forcing your clinical team to double as financial collectors. Free them to do what they do best: care for your patients.

Ready to see how a dedicated Virtual Medical Assistant can professionally manage your patient collections, improve your cash flow, and give your staff their valuable time back?

Take Control of Your Revenue Cycle Today.

Let our trained VMAs handle the complexities of patient collections with the empathy and efficiency your practice deserves.